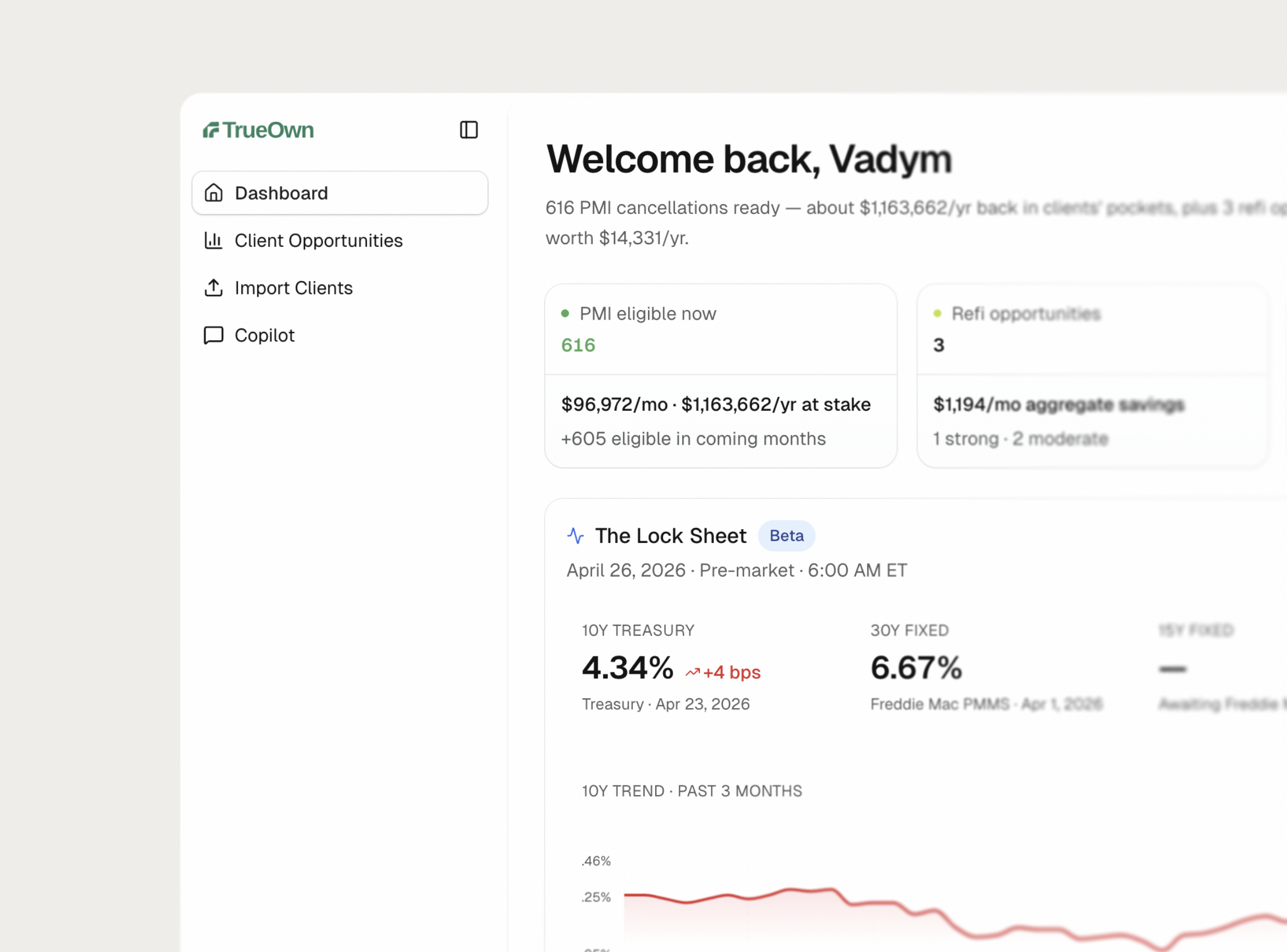

Some of your past clients already left. We name them.

Every refi is a recorded deed. We pull mortgage history per address — new lender, date filed.

Refied elsewhere

Public deed records · refreshed weekly

23 of 312

past clients refinanced with another lender

- Patel, R.NewRez · Aug 2024

- Cohen, S.loanDepot · Mar 2025

- Reyes, A.PennyMac · Jan 2026

- + 20 more

- First detected

- Mar 2022

- Most recent

- Feb 2026

- Top new lender

- NewRez

- Avg time to leave

- 28 mo

Sourced from county recorder filings via ATTOM. No homeowner action required.